Headline inflation in May 2026 sits at 3.8%, but the price tags American shoppers see at the register tell a different story. Ground coffee is up 31% year over year. Beef and veal are up 12%. A 12-pack of soda costs nearly double what it did in 2020. After more than a year of compounding hikes, shoppers are walking away from brands they once stood by.

To measure how 2026 price pressure is affecting consumer behavior, DOSS surveyed 1,010 U.S. adults about brand loyalty, product category pain, and shopping habits. We found that loyalty breaks at a much lower price threshold than companies might assume, grocery aisles take the heaviest hit, and discount grocers are gaining shoppers while traditional supermarkets shed them.

Key Takeaways

- 60% of Americans have dropped a brand they were loyal to because of 2026 price increases.

- Ground coffee is up 31% year-over-year, from $7.22 to $9.46 per pound. The single steepest Consumer Packaged Goods (CPG) price move of 2026, running more than eight times the headline Consumer Price Index (CPI) rate of 3.8%.

- The breaking point is just a 16% price hike, on average. That's all it takes for the median shopper to switch to a cheaper brand, less than half what it takes to stop buying altogether (33%).

- Groceries are where inflation cuts deepest in 2026: 82% of Americans say food and beverage prices hurt most, followed by gas and fuel at 76%.

- Aldi and Lidl are winning the 2026 inflation economy: 41% of Americans shop at discount grocers more than they did a year ago, while 38% shop at traditional supermarkets less.

- 69% of Americans say store brand products are just as good as name brands, and the most common move after dropping a loyal brand was switching to a generic version (53%).

Brand Loyalty Cracks Long Before Shoppers Walk Away

- 60% of Americans say they have dropped a brand they were previously loyal to because of 2026 price increases. The break is more common among younger, female, and lower-income shoppers:

- 61% of Gen Z and millennials have dropped a brand, compared with 58% of baby boomers and 57% of Gen X.

- Women (62%) are more likely than men (56%) to have made the switch.

- 62% of those earning under $25K have done so vs. 52% of those earning $100K or more.

- On average, a 16% price increase is enough to push shoppers toward a cheaper name brand, a private label, or a smaller quantity, with the median sitting at just 10%. Baby boomers will switch to a cheaper brand at an average 12% increase, while Gen Z and millennials hold out until 17%.

- Walking away from a product entirely takes a 33% increase on average, and a 25% increase at the median.

- Among the 601 Americans who dropped a loyal brand, 76% did so on groceries, followed by personal care (41%), household goods (39%), and dining out (39%).

- 27% dropped a subscription service, and 14% each dropped a pet food or gas brand.

- 85% of brand-droppers earning under $25K dropped a grocery brand, compared with 72% to 76% across higher income brackets.

- After dropping a loyal brand, 53% of Americans switched to a generic version, 52% to a cheaper name brand, 48% to a private label or store brand, and 41% stopped buying that type of product altogether.

- 70% of Americans say they are less brand loyal than a year ago, and 69% say store brand products are just as good as name brands. Gen Z is the only generation where store-brand acceptance trails the rest at 64%, compared with 70% for millennials, Gen X, and baby boomers.

Inflation Pain Drives Shoppers Toward Discount Retailers

- 82% of Americans say food and beverage prices are among the most painful for them right now, followed by gas (76%), utilities (46%), and dining out (42%). Household goods (28%), housing (24%), and auto-related costs (22%) round out the top categories.

- 85% of baby boomers and Gen X cite groceries as one of the most painful categories, compared with 82% of millennials and 74% of Gen Z.

- Housing pain peaks among shoppers earning $25K to $49K (29%) and bottoms out among those earning $100K or more (20%).

- Dining out is the single biggest casualty of 2026 inflation: 62% of Americans have cut back on it, followed by vacations (48%), entertainment (47%), social outings and date nights (44%), hobbies (38%), and higher-quality groceries (38%).

- 30% have also cut savings or retirement contributions.

- 46% of Americans earning under $25K have cut back on healthier groceries, nearly twice the rate of those earning $100K or more (24%).

- Looking at net change in shoppers over the past year, discount grocers gained 30 points (41% shop there more, 11% less), dollar stores gained 20 points, and warehouse clubs like Costco gained 4 points.

- Mass retailers like Walmart and Target were roughly flat (-1), online retailers like Amazon lost 17 points, and traditional supermarkets like Kroger and Publix lost 28 points.

- The migration to discounters is led by younger shoppers: 44% of millennials and 43% of Gen Z shop discount more than a year ago, compared with 35% of Gen X and 34% of baby boomers.

- Because of inflation, 68% of Americans say they feel frustrated when they shop, 51% feel anxious, 35% feel helpless, and 28% feel resigned. Another 39% feel motivated to find better deals, and 18% feel embarrassed about what they can no longer afford.

- 72% of women feel frustrated, and 56% feel anxious, compared with 64% and 43% of men.

- 40% of Americans earning under $25K feel helpless when shopping, compared with 27% of those earning $75K to $99K.

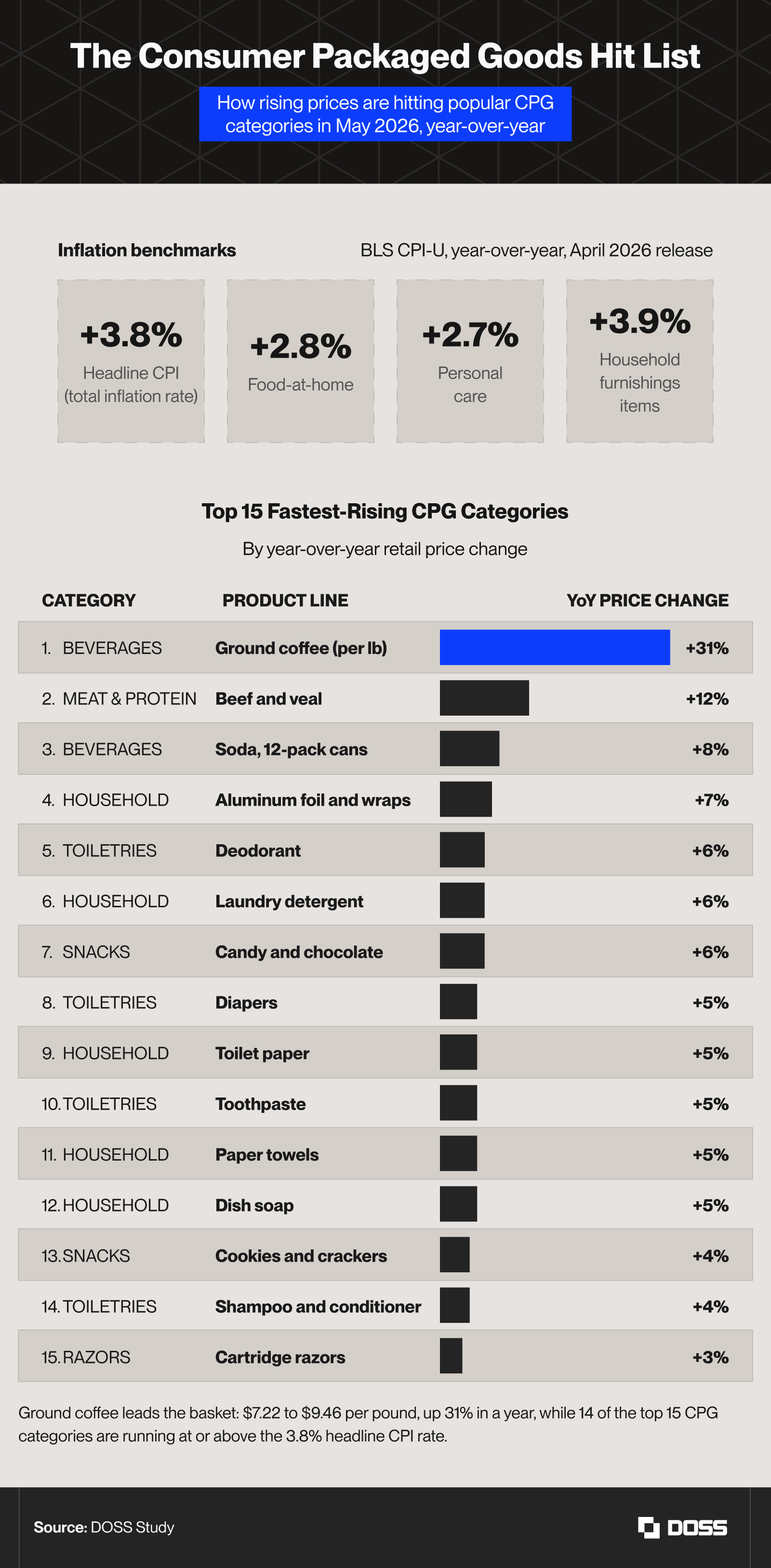

CPG Prices Outpace Headline Inflation Across Most Categories

- The 3.8% headline CPI rate understates what Americans see at the shelf. For context, the relevant BLS year-over-year benchmarks are:

- Food at home +2.8%

- Personal care +2.7%

- Household furnishings and items +3.9%

- Meats and poultry +5.6%

- Nonalcoholic beverages +4.6%

- 14 of the top 15 fastest-rising CPG categories are running at or above that total inflation rate, and only cartridge razors (+3%) sit below it.

- Ground coffee is the single steepest CPG move of 2026. Retail prices jumped from $7.22 to $9.46 per pound year over year, a 31% increase.

- Beef and veal are up 12% year over year.

- Soda is the most-cited "feels expensive" SKU at the grocery store: a 12-pack of cans is up 8% year over year and 89% cumulatively since 2020 ($5.18 to $9.79 on average).

- Cocoa is the snack-aisle culprit: cocoa futures hit all-time highs in 2024 and 2025 , and Mondelez took 8% pricing across FY 2025 on cocoa cost pass-through, which drove organic revenue +4.3% on volume -3.7%. At retail, candy and chocolate are up 6%, and cookies and crackers are up 4%.

- Shrinkflation is the unspoken hike. A 2025 industry estimate puts the average effective price increase from documented pack-size reductions at roughly 14.8% across surveyed national grocery brands.

- 75% of U.S. consumers say they have noticed shrinkflation, and among those, 81% are taking action.

Methodology

We surveyed 1,010 U.S. adults in May 2026 via SurveyMonkey Connect on the Prolific panel to measure how 2026 inflation is changing American brand loyalty, category-level pain points, and shopping behavior.

- Gender: 54% women, 45% men, 1% non-binary or not listed

- Generation: 49% millennials (age 30 to 45), 25% Gen X (46 to 61), 17% Gen Z (18 to 29), 10% baby boomers (62+)

- Personal annual income, before taxes: 24% under $25K, 25% $25K to $49K, 22% $50K to $74K, 14% $75K to $99K, 14% $100K or more

- Household size: 21% one person, 33% two people, 33% three to four people, 12% five or more

The CPG Hit List ranks 15 product lines by unadjusted year-over-year change in U.S. retail prices, comparing April 2026 against April 2025. Figures combine BLS CPI category data, USDA ERS Food Price Outlook estimates, and disclosed pricing actions from major manufacturers' earnings releases and trade press through Q1 2026. The benchmark strip above the table shows headline CPI and three CPG-adjacent aggregates, so each row can be read as above or below trend. The sticker-price changes shown here do not capture shrinkflation, which adds an estimated ~15% effective increase to a subset of these items.

About DOSS

DOSS is the Operations Cloud built for the real world: a modern, AI-native platform that helps product-based businesses manage the flow of goods, dollars, and data across procurement, inventory, orders, fulfillment, and finance in real time. With composable modules and a unified master data model, DOSS helps operations teams adapt faster to volatility and make confident decisions when costs shift unexpectedly. Learn more at www.doss.com .

Fair Use Statement

The data and insights in this article may be used for noncommercial purposes only. If shared, please provide proper attribution to DOSS.